Help your clients reach their goals by staying on top of the economy, markets, and investment strategies. Simply tap into timely insights and analysis from our senior leaders, economists, and investment experts.

In the wake of pandemic shocks, economies appear more “normal” than at any time since 2019. Yet policy rates remain elevated. As central banks cut interest rates to more neutral levels, key questions include how fast they get there and what those neutral levels will look like. Here are our near-term economic views:

The factors that supported relative U.S. economic strength are diminishing. That suggests some recoupling with the rest of the world and further progress on curbing inflation.

Developed markets (DM) appear on track to return to target inflation levels in 2025, driven by normalizing consumer demand and increased competition for limited job openings. In the U.S., labor markets appear looser than in 2019, heightening the risk of rising unemployment. The Fed, like other DM central banks, is expected to realign monetary policy to this new cyclical reality.

The U.S. economy, like others, appears poised to achieve a rare soft landing – moderating growth and inflation without recession. But there are risks, such as the upcoming U.S. election and its implications for tariffs, trade, fiscal policy, inflation, and economic growth. High budget deficits will likely persist, limiting the potential for further fiscal stimulus and adding to economic risks.

As developed economies slow and potential trade and geopolitical conflicts loom, investors should favor caution and flexibility in portfolio positioning. These are our near-term investment views:

We expect yield curves to steepen as central banks lower short-term rates, creating a favorable environment for fixed income investments. Historically, high quality bonds tend to perform well during soft landings and even better in recessions. Moreover, bonds have recently resumed their traditional inverse relationship with equities, providing valuable diversification benefits.

Bond yields are attractive in both nominal and inflation-adjusted terms, with the five-year area of the yield curve particularly appealing. Cash rates are set to decline alongside policy rates, while high government deficits may drive long-term bond yields higher over time.

We maintain a cautious stance given some complacency we see in corporate credit due to tighter valuations, favoring higher-quality credit and structured products. Lower-quality, floating-rate private market areas appear more vulnerable to economic downturns and interest rate changes than prices suggest, with credit risks poised to rise just as yields fall, potentially benefiting borrowers but hurting investors. U.S. agency mortgage-backed securities (MBS) offer an attractive and liquid alternative to corporate credit.2

In private credit markets, we believe that excessive growth and complacency are likely to result in weaker future returns when compared with current yield levels. Significant capital formation has resulted in weaker lender protections and compressed compensation for illiquidity relative to similar returns available to active managers in public credit markets.

We believe many lower-quality, floating-rate borrowers in private markets are more susceptible to economic weakness and interest rate changes than market prices suggest. As the Fed lowers rates to prevent a recession, floating-rate coupons will likely also decrease significantly. This means yields will drop just as economic and credit risks rise, which may benefit borrowers but hurt investors. This could also be the first time these markets are tested during economic downturn scenarios.

Given this backdrop, investors today may be receiving inadequate compensation for risk in lower-quality private corporate credit – especially compared with attractive excess return opportunities in more liquid forms of credit or similarly less liquid opportunities in asset-based lending. (For more, see our 10 July 2024 publication, “Navigating Public and Private Credit Markets: Liquidity, Risk, and Return Potential”).

Disruption to bank business models is creating attractive entry points for private capital across a range of asset-based opportunities, including consumer-related (e.g., residential mortgages, student loans) and non-consumer (e.g., aviation, equipment) assets. Relative to private corporate markets, we find many asset-based opportunities benefit from a combination of attractive starting valuations and favorable fundamentals, especially in areas tied to the higher-quality consumer balance sheet. These markets are also less crowded on a relative basis, as capital formation in private asset-based lending remains considerably more scarce than that of U.S. and European corporate lending markets.

We believe we are closer to a bottom in private real estate markets, but that this will be a slower recovery relative to previous cycles. We favor investments in data infrastructure and debt-related opportunities relative to equity at current valuations. Our emphasis is on sectors and assets tied to data infrastructure, logistics, warehouses, and certain multifamily assets.

Global views

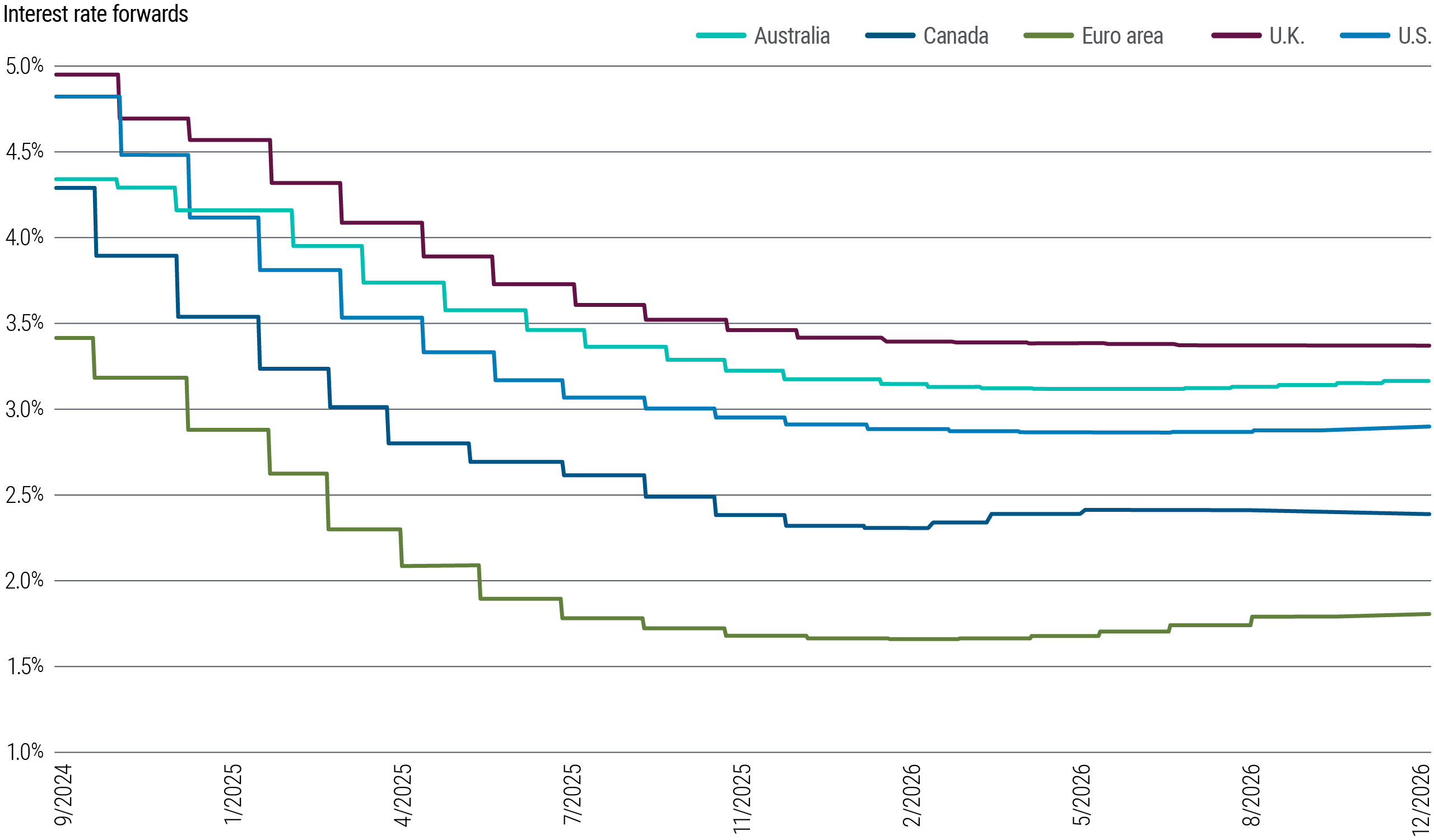

Given dispersion in economic outlooks and central bank policy paths, we favor duration positions in the U.K. and Australia, where terminal pricing for the central bank cycles (see Figure 3) still looks somewhat high versus the U.S., the eurozone, and other global markets.

Figure 3: Market expectations vary for central bank policy rate trajectories and terminal levels

Source: Bloomberg data and PIMCO calculations as of 30 September 2024

In the eurozone, the market’s terminal rate pricing for the European Central Bank looks reasonable, but there is some uncertainty on the timing of how quickly the easing cycle proceeds. Overall, we are neutral on duration but favor curve steepening positions given the flatness of the curve between the 10- and 30-year points.

Looking at foreign exchange (FX), we prefer an underweight position in the U.S. dollar, given risk of weakening as the Fed lowers rates, while diversifying with EM and DM positions. Careful scaling of positions is needed here, however, given the uncertainties surrounding the U.S. election.

A stable-to-weaker U.S. dollar amid rate-cutting cycles across DM should enable EM central banks to cut rates as well. While the Fed was on hold, many of these central banks had to keep rates higher than their benign domestic inflation would normally require.

We prefer investments in markets with steep yield curves and stable or improving political conditions, such as South Africa and Peru. Turkey also remains of interest given the ongoing pivot to greater economic orthodoxy. The favorable global environment we expect should remain supportive of EM external debt spreads.

Certain commodities can help diversify portfolios and provide hedging properties against inflation risks. The shifting global landscape continues to support gold and precious metals, with EM central banks purchasing gold at unprecedented rates since Russia’s invasion of Ukraine. Meanwhile, the desire of OPEC+ to return supply to the market and concerns over global transport demand have limited the upside to oil prices, even as recent events in the Middle East and Ukraine underscore the fragility of global supply chains. The capital spending cycle linked to the energy transition also supports prices of base metals, although lingering downside risks to growth in China pose challenges.